Tally Review 2026: Is Tally Worth It for Debt Management?

Discover whether Tally is still worth using in 2026 for managing credit card debt. This detailed review explores its features, pricing, pros and cons, and current availability, helping you decide if Tally is the right solution for your debt management needs.

Table of Contents

What is Tally and How Does It Work?

Core Concept of Tally

If you’ve ever felt overwhelmed juggling multiple credit card bills, you’re not alone. That’s exactly where Tally stepped in as a financial lifesaver. At its core, Tally was designed to simplify debt repayment by combining all your credit card balances into one manageable system. Instead of tracking multiple due dates, interest rates, and minimum payments, you just deal with one streamlined platform.

The idea is simple but powerful: Tally connects to your credit cards, analyzes your balances, and then creates a strategic repayment plan. It focuses on reducing interest costs and helping you pay off debt faster. According to financial reports, Tally typically prioritized high-interest debt first, similar to the debt avalanche method, which is one of the most efficient repayment strategies.

This approach made it appealing for users drowning in high-interest credit card debt. Rather than manually deciding which card to pay first, Tally handled the decision-making for you. It’s like having a financial assistant working behind the scenes, constantly optimizing your payments.

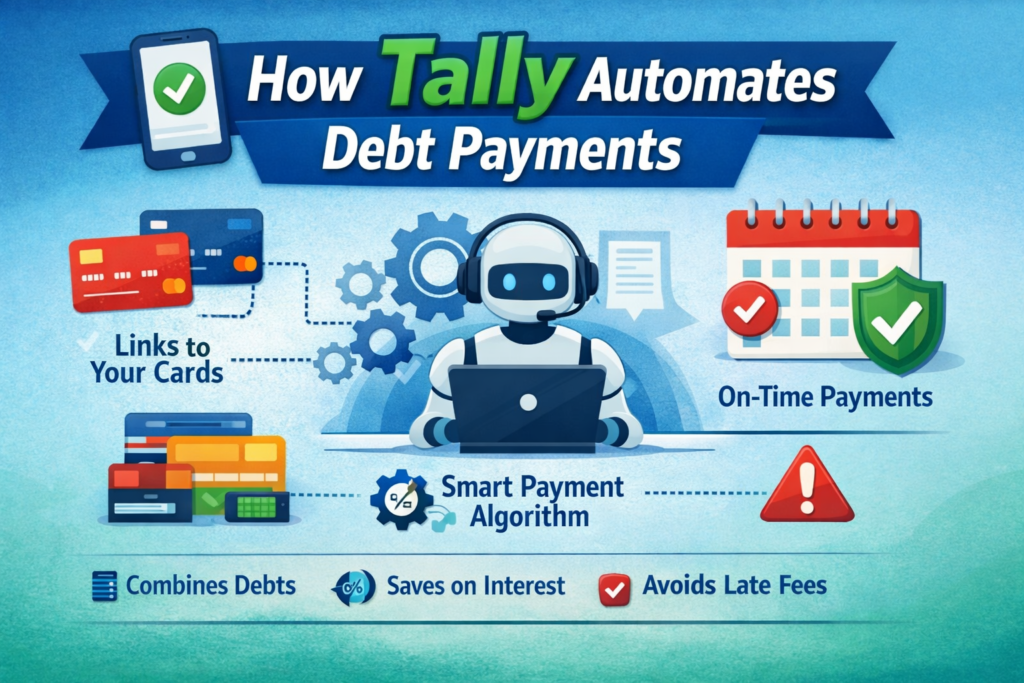

How Tally Automates Debt Payments

Tally didn’t just organize your debt—it actively managed it. Once you linked your accounts, the app would automatically make payments on your behalf. This automation ensured you never missed a due date, helping you avoid late fees and protect your credit score.

The platform used intelligent algorithms to determine how much to pay and where. For example, it would pay more toward high-interest cards while maintaining minimum payments on others. This kind of automation reduced both stress and human error.

Even better, Tally offered late fee protection, meaning it could step in and make minimum payments if you forgot. For many users, this feature alone was worth it, especially if they had a history of missed payments.

Tally Pricing and Plans (2026 Update)

Free Membership

Tally offered a free version that allowed users to track debt and get reminders. This plan was ideal for those who didn’t qualify for the credit line but still wanted help organizing their finances.

Tally Basic

This plan was free upfront, but you paid interest on the credit line. APR ranged from 7.90% to 29.99%, making it competitive compared to credit cards.

Tally+

Tally+ cost around $300 per year and offered:

- Lower APR

- Larger credit line

- Additional financial insights

Key Features of Tally

Debt Consolidation

One of Tally’s standout features was its ability to consolidate multiple credit card debts into a single payment. Instead of paying five different cards, you made one payment to Tally. This not only simplified your finances but also helped reduce confusion and missed deadlines.

Automatic Payments

Automation is where Tally truly shined. It handled your monthly payments, ensuring that each card received the right amount at the right time. This feature was particularly useful for busy individuals who didn’t want to track multiple due dates.

Line of Credit System

Tally offered a line of credit to pay off your credit cards. You then repaid Tally instead of your card issuers. Interest rates ranged between 7.90% and 29.99% APR, depending on your creditworthiness.

Smart Payoff Strategies

Tally used proven methods like:

- Debt avalanche (pay highest interest first)

- Debt snowball (smallest balance first)

These strategies helped users save money and pay off debt faster.

Pros and Cons of Tally

Advantages

Tally offered several benefits that made it attractive for debt management. First, it simplified finances by consolidating multiple payments into one. This alone reduced stress and improved financial clarity. Second, automation ensured timely payments, helping users avoid costly late fees.

Another major advantage was potential interest savings. If Tally’s APR was lower than your credit cards, you could save a significant amount over time. The app also performed a soft credit check, meaning it didn’t harm your credit score during application.

Disadvantages

However, Tally wasn’t perfect. One major drawback was the credit score requirement, typically around 580 or higher. This excluded many users.

Additionally, not all credit cards were supported, and availability was limited to certain regions. Another concern was that users were still taking on debt—just in a different form. If not managed properly, this could lead to prolonged repayment periods.

Is Tally Still Available in 2026?

Service Changes After 2024

Here’s the biggest update you need to know: Tally shut down its direct consumer operations in 2024. This means the original app is no longer available in the same form.

Partner-Based Model

Tally has shifted toward a partner-based platform, integrating its technology with financial institutions instead of offering direct services. This means you may still encounter Tally-powered tools, but not the standalone app.

Who Should Use Tally?

Ideal Users

Tally was best suited for:

- People with multiple credit card debts

- Users struggling with high interest rates

- Individuals who prefer automation

Who Should Avoid It

It wasn’t ideal for:

- People with low credit scores

- Users who pay full balances monthly

- Those seeking zero-interest solutions

Tally vs Other Debt Management Apps

Feature Comparison Table

Feature | Tally | Debt Payoff Planner | Bright Money |

Automation | Yes | Limited | Yes |

Line of Credit | Yes | No | No |

Cost | Free + interest | Free/$2 | $6.99+ |

Strategy Tools | Advanced | Basic | AI-based |

Availability | Limited | Global | Global |

Also Read

Savvy Car Insurance Savings: How to Reduce Your Premiums Easily

TransferGo: Fast and Affordable International Money Transfers Guide

MYOB: Complete Accounting Software Guide for Businesses

Banggood: Complete Online Shopping Guide for Deals and Discounts

Drop: The Ultimate Platform for Exclusive Tech & Gear Deals

Real User Reviews and Feedback

User feedback for Tally has generally been positive. Many users appreciated the automation and simplicity. According to customer reviews, the app was “easy to use” and effective in managing multiple debts.

However, some users reported issues with eligibility and limited availability. Others mentioned that while Tally helped organize debt, it didn’t eliminate the underlying financial habits causing the debt.

Is Tally Safe and Secure?

Security is always a concern when dealing with financial apps. Tally used bank-level encryption and did not store sensitive banking information.

This made it relatively safe, but like any financial tool, users needed to exercise caution and follow best practices.

Alternatives to Tally in 2026

Since Tally is no longer widely available, here are some alternatives:

- Debt Payoff Planner

- Bright Money

- Undebt.it

These apps offer similar features like tracking, planning, and automation.

Conclusion

Tally was once a powerful tool for managing credit card debt. Its automation, consolidation, and smart strategies made it stand out in a crowded market. For users who qualified, it could significantly reduce interest costs and simplify financial management.

But here’s the reality in 2026: Tally is no longer available as a standalone app. That changes everything. While its technology may still exist through partners, the original experience is gone.

So, is Tally worth it? If it were still fully operational, the answer would likely be yes for many users. But today, your best option is to explore alternatives that offer similar benefits with broader availability.

Frequently Asked Questions

No, Tally shut down its direct consumer app in 2024 and now operates through partners.

Its combination of automation, debt consolidation, and a line of credit made it stand out.

Yes, but users paid interest on the credit line and optional membership fees.

Typically, a minimum score of around 580 was needed.

Apps like Bright Money and Debt Payoff Planner are popular alternatives.

Table of Contents

Popular Posts

-

Affordable Technical SEO Audit for Small Business: A Complete Guide26 Jun 2025 Blog

Affordable Technical SEO Audit for Small Business: A Complete Guide26 Jun 2025 Blog -

How to Get an Affordable Technical SEO Audit for Small Business27 Jun 2025 Blog

How to Get an Affordable Technical SEO Audit for Small Business27 Jun 2025 Blog -

The Ultimate Local SEO Audit Checklist for Startups28 Jun 2025 Blog

The Ultimate Local SEO Audit Checklist for Startups28 Jun 2025 Blog -

Local SEO Audit Checklist for Startups: A Beginner’s Guide28 Jun 2025 Blog

Local SEO Audit Checklist for Startups: A Beginner’s Guide28 Jun 2025 Blog -

Top On-Page SEO Audit Steps for Service Websites Every Business Should Know29 Jun 2025 Blog

Top On-Page SEO Audit Steps for Service Websites Every Business Should Know29 Jun 2025 Blog -

The Impact of On-Page SEO Audit Steps for Service Websites on UX01 Jul 2025 Blog

The Impact of On-Page SEO Audit Steps for Service Websites on UX01 Jul 2025 Blog -

Technical SEO for WordPress: The Ultimate Beginner’s Guide01 Jul 2025 Blog

Technical SEO for WordPress: The Ultimate Beginner’s Guide01 Jul 2025 Blog -

Technical Mobile SEO Audit Tips for Developers02 Jul 2025 Blog

Technical Mobile SEO Audit Tips for Developers02 Jul 2025 Blog

Related Post